The latest Strait of Hormuz blockade threat is back at the center of global markets, and the price action says investors are taking it seriously. Brent and WTI both climbed back above $100 a barrel on April 13 after President Donald Trump said the U.S. Navy would begin blockading vessels linked to Iranian ports, a sharp escalation after weekend talks with Tehran failed to produce a deal. Reuters reported oil jumped roughly 8% in early trading, while CNBC said the move risks deepening what is already the worst energy shock in years Reuters via EnergyNow CNBC.

This isn't just another geopolitical scare headline. It hits the world's most sensitive oil chokepoint, one that carries about a fifth of global petroleum flows. When traders hear "Hormuz," they don't think theory. They think immediate supply risk, freight dislocation, and a fresh inflation problem.

Oil's move above $100 reflects fear, not just lost barrels

The market had briefly hoped the two-week ceasefire announced on April 8 would reopen the waterway in a meaningful way. That optimism now looks premature. Reuters reported on April 10 that analysts were already warning the Iran war could flip the oil market from expected oversupply into deficit this year, erasing a much softer outlook for 2026 Reuters.

The U.S. Energy Information Administration has also acknowledged how exposed the market is. In its April 7 release, the EIA said its forecasts depend heavily on how long disruption in the Strait lasts, and under a scenario where the conflict does not persist past April, shut-in production would still remain elevated into May before gradually easing later in 2026 U.S. EIA.

That matters because the current price spike is not only about Iranian barrels. It reflects the risk premium attached to every Gulf export cargo, every tanker route, and every refinery that depends on predictable flows from the region.

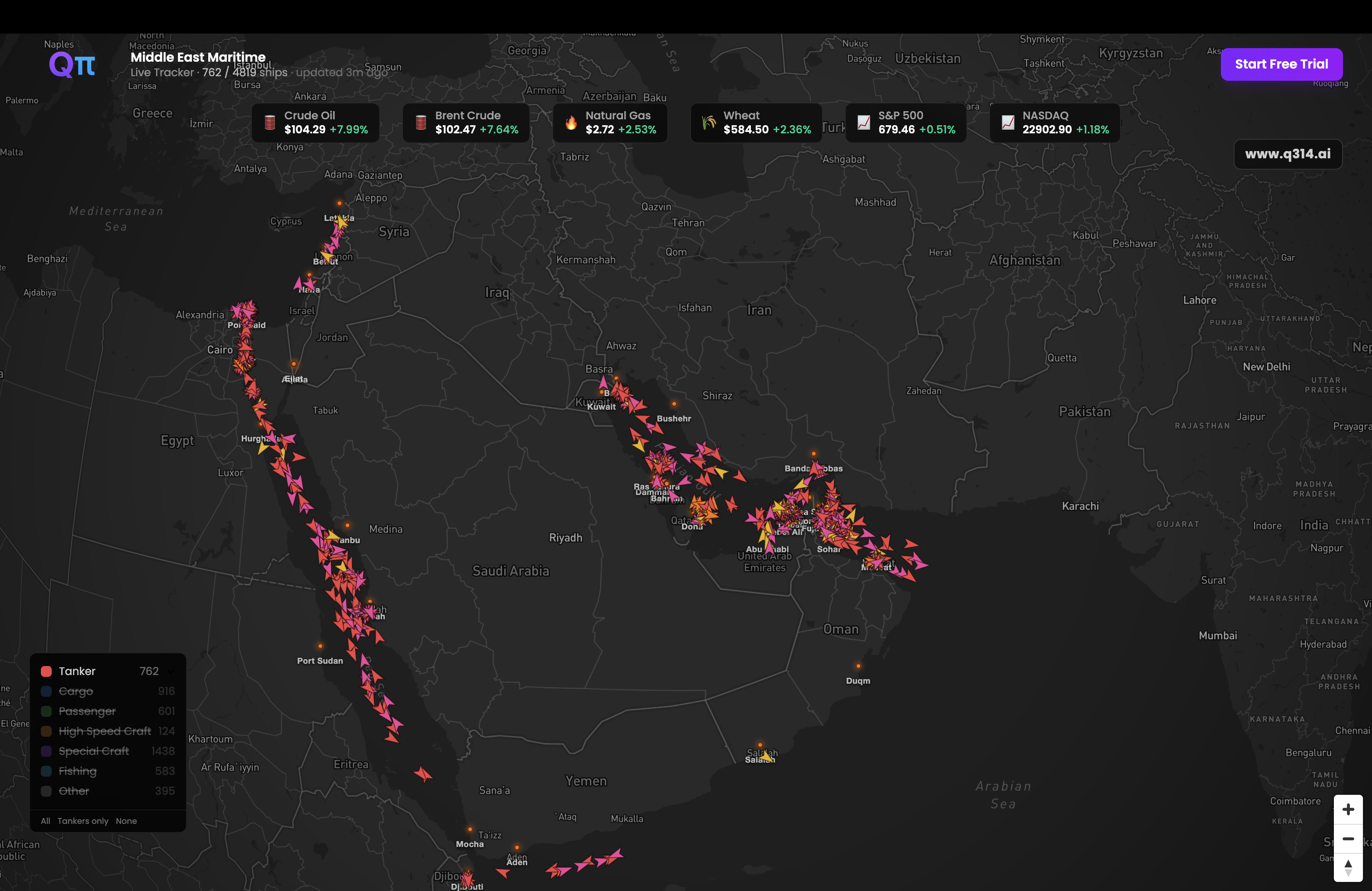

Shipping through the Strait is moving, but only barely

Even before the latest U.S. blockade announcement, shipping was nowhere near normal. Reuters reported on April 11 that three fully laden supertankers managed to exit the Gulf, appearing to be the first such departures since the conflict sharply disrupted traffic. That was a sign of limited movement, not a return to business as usual Reuters.

CNBC went further on April 9, citing analysts who said tanker traffic may take weeks or even months to recover even if a ceasefire technically remains in place. Owners, insurers, and charterers need clarity on routing, security guarantees, and war-risk premiums before they send ships back at scale CNBC.

The Financial Times has reported similar skepticism in the shipping market, with conventional traffic still constrained and operators questioning official claims that passage is opening up in a durable way Financial Times.

Why Asia is especially exposed to the latest Hormuz shock

The immediate economic pain won't be evenly distributed. Asia is the most vulnerable because China, India, Japan, and South Korea all rely heavily on Gulf crude and LNG. CNBC noted that a tougher U.S. posture in Hormuz risks piling pressure on major Asian importers just as they were trying to manage the fallout from the broader Iran conflict CNBC.

That has a second-order effect for traders. If Asian buyers scramble for replacement barrels, Atlantic Basin crude grades, diesel cracks, LNG benchmarks, and tanker rates all become part of the same trade. The shock doesn't stay local for long.

What traders should watch next

The next signal is not the next political statement. It's whether physical flows improve. Watch tanker transits, war-risk insurance costs, and whether more loaded vessels actually clear the Strait over the next several sessions. If traffic remains thin while crude holds above $100, the market will start pricing not a temporary scare, but a longer supply regime shift.

Actionable insight: traders should treat this as a cross-asset event, not just an oil headline. Crude, refined products, tanker stocks, inflation trades, and Asian import-sensitive equities are now linked. If Hormuz traffic fails to normalize this week, the cleaner trade may be to stay long volatility and favor products and freight over outright crude, because the bottleneck is increasingly about movement, not just production.